Ticker: CLS

Price: 337.9 USD

Target: 425 USD

Closed: 401.66 USD

Company Overview

Celestica Inc. is a global provider of advanced supply chain, design and manufacturing solutions, serving customers across Asia, North America and international markets. The company was incorporated in 1994 as a subsidiary of IBM (later spun off in 1996) and is headquartered in Toronto, Canada. Celestica has evolved from a traditional electronics manufacturing services (EMS) provider into a higher-value, solutions-oriented partner focused on complex, mission-critical and cloud-centric systems.

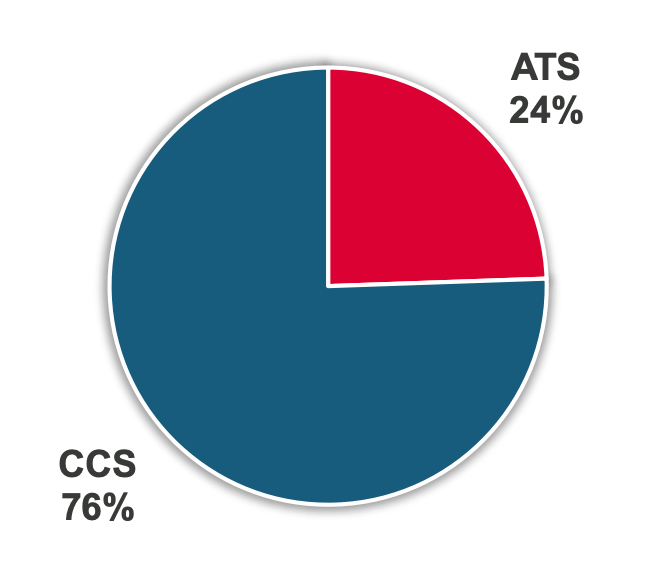

Celestica operates through two reportable segments: Advanced Technology Solutions and Connectivity and Cloud Solutions.

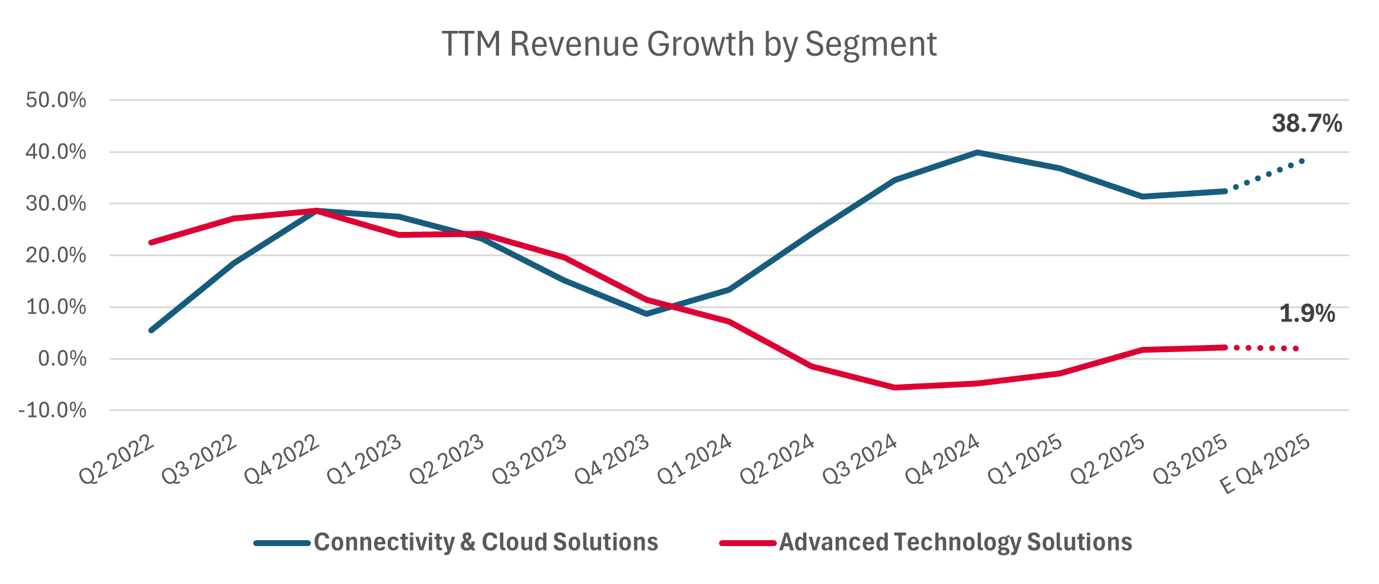

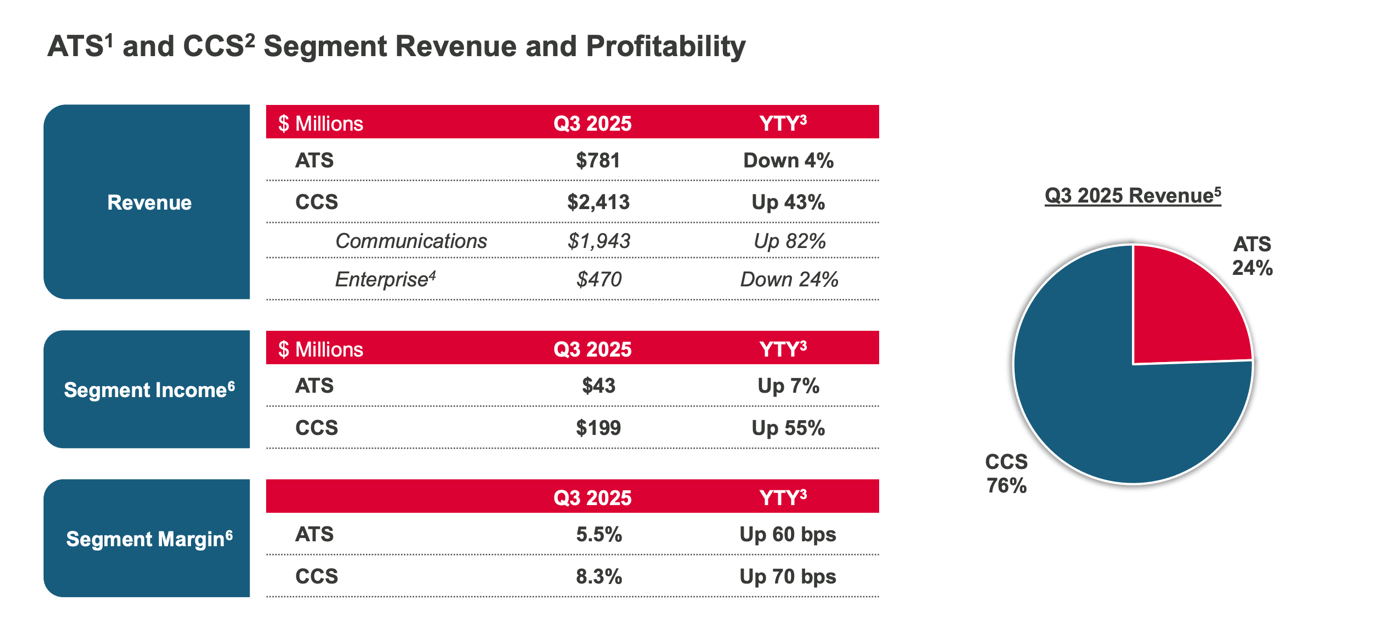

As of the most recent quarter, Connectivity and Cloud Solutions accounted for approximately 76% of total revenue, while Advanced Technology Solutions contributed roughly 24%, reflecting the company’s increasing exposure to hyperscale cloud and AI infrastructure.

Together, these segments reflect a deliberate strategic shift toward end-to-end product lifecycle management, combining engineering, platform design, manufacturing, and aftermarket services to reduce customer time-to-market and operational complexity.

The company’s customer base includes original equipment manufacturers, hyperscalers, cloud service providers and enterprises operating across aerospace and defense, industrial, HealthTech, capital equipment, communications and enterprise end markets.

Business Model and Segment Overview

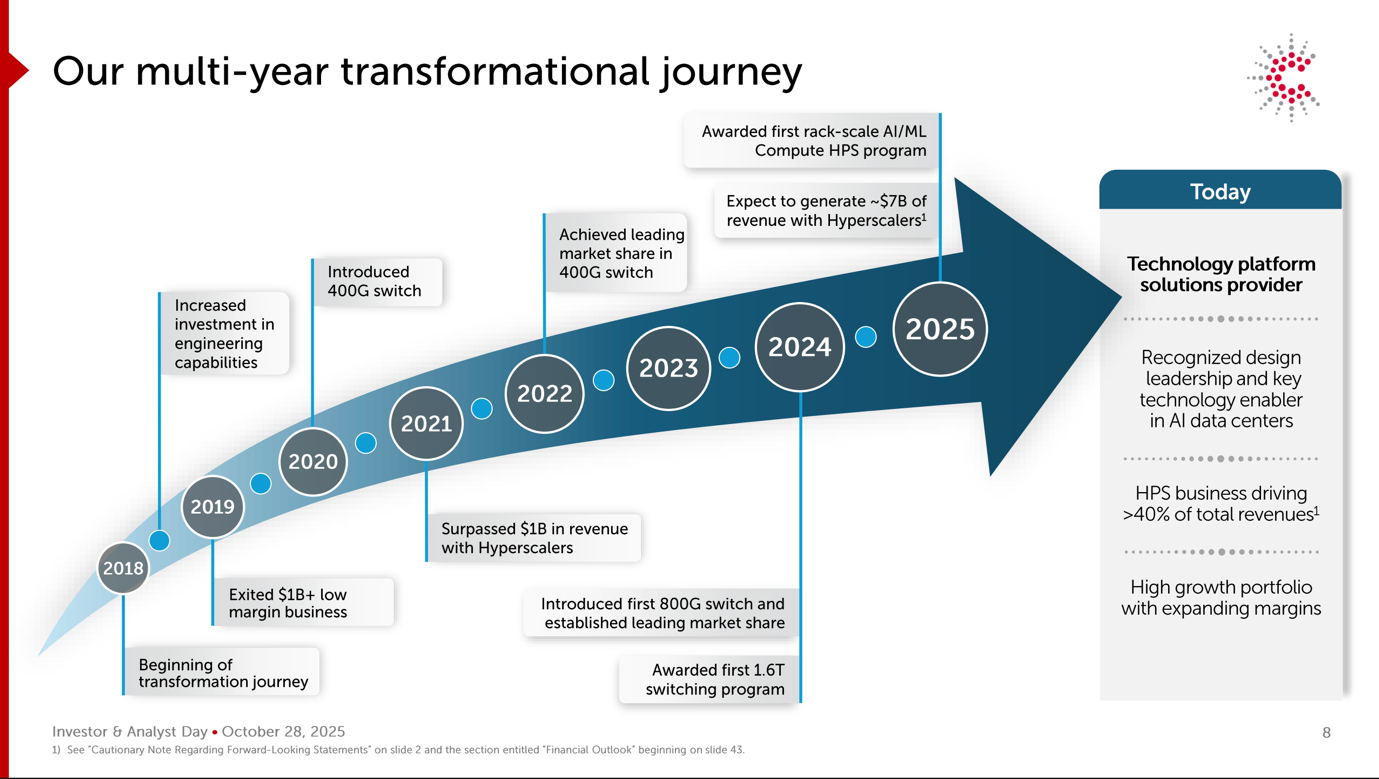

Celestica has changed its business model over time, moving from spot contracts (with third-party customers outside IBM) to a Customer Lifetime Value-driven paradigm. The company now has an improved profitability profile (with operating margins growing from 5% in 2019 to 8% in 2025) and has extended the average duration of its contracts. The increase in backlog provides greater visibility on future revenues, allowing the management to see grow rates of 40% in the CCS segment well into 2027.

Advanced Technology Solutions (ATS) focuses on markets where product complexity, reliability and regulatory compliance are critical, including aerospace and defense, industrial applications and medical technology. This segment accounts for 24% of revenues and 18% of operating income, due to operating margins being lower than the CCS segment. Through its Advanced Technology Solutions, Celestica acts as an integrated manufacturing and engineering partner, providing design and development, new product introduction, precision machining, advanced testing, systems integration and full aftermarket support. These programs typically feature longer product lifecycles, high switching costs and greater revenue visibility, supporting margin stability and lower cyclicality relative to traditional EMS activities.

Connectivity and Cloud Solutions (CCS) is the company’s primary growth engine and its most direct exposure to secular trends in cloud computing, hyperscale data centers and artificial intelligence. This segment accounts for 76% of total revenues and generates 82% of operating income, thanks to higher profitability margins (8.3% vs 5.5% in ATS). Through CCS, Celestica delivers customized hardware platform solutions, including servers, storage and networking systems designed for specific workloads. A key differentiator is the company’s capability in open hardware and open software architectures, enabling customers to reduce vendor lock-in while optimizing performance and cost. Celestica supports these platforms across the full lifecycle, from design and supply chain orchestration to manufacturing, deployment and asset management.

Importantly, engineering capabilities developed within ATS increasingly support advanced CCS programs, particularly in high-performance and mission-critical cloud infrastructure, reinforcing Celestica’s competitive positioning versus volume-driven EMS peers.

CCS drives revenue growth and operating leverage, while ATS provides margin stability and visibility.

Competitive Positioning

Celestica occupies a differentiated position within the EMS landscape, competing less on pure assembly volume and more on technical complexity, customization and full product lifecycle integration. Rather than acting as a commoditized manufacturing vendor, the company increasingly positions itself as a strategic partner, embedding engineering, platform design and supply chain orchestration early in the product development process.

This approach allows Celestica to capture a greater share of the overall system value, increases switching costs for customers and reduces exposure to pricing pressure typically associated with volume-driven EMS models. As a result, the company has been able to structurally improve margin quality, generate more consistent free cash flow and maintain disciplined working capital management. Long-term relationships with hyperscalers, as well as customers in aerospace, defense and industrial markets, further enhance revenue visibility and customer retention, supporting a more resilient earnings profile across cycles.

Industry Analysis

The Electronics Manufacturing Services (EMS) sector comprises companies that design, assemble, and manage the production of electronic systems on behalf of third parties. These firms do not sell products under their own brands, but instead operate as industrial partners to large technology and industrial groups that retain control over branding, software, and end-customer relationships.

Historically, the EMS industry emerged primarily as a cost-reduction tool. Manufacturing activities were outsourced to take advantage of lower labor costs and scale efficiencies, particularly within Asian production hubs. Under this traditional model, EMS providers played a largely execution-oriented role: they received fully defined product designs from customers, assembled the hardware, and delivered finished units. The resulting economic profile was characterized by thin margins, intense price competition, and limited ability to influence profitability.

Over time, however, increasing hardware complexity and accelerating technology cycles have made this model progressively less sustainable. By 2026, the EMS sector is no longer a homogeneous industry, but a fragmented ecosystem encompassing materially different business models. The key distinction is no longer simply between companies that manufacture and those that do not, but between those that control a technological platform and those that merely provide manufacturing capacity.

Within this context, the distinction between traditional EMS and more advanced models such as Joint Design Manufacturing (JDM) and Original Design Manufacturing (ODM) has become increasingly important.

Under JDM and ODM frameworks, the manufacturing partner does not simply assemble a pre-defined product, but actively participates in hardware design, architectural definition, and in some cases retains partial ownership of the underlying intellectual property. This approach materially increases customer switching costs, as relocating production to an alternative supplier becomes complex, costly, and operationally risky. From an economic standpoint, these models support higher margins and greater revenue visibility than traditional EMS arrangements.

A second critical dimension for understanding the EMS sector in 2026 is business mix. Broadly speaking, the market can be divided into two major areas. On one side are connectivity and cloud-related segments, including servers, networking equipment, and data center infrastructure. These markets are characterized by high volumes, strong exposure to hyperscaler capital expenditure cycles, and structurally lower margins. On the other side are high-reliability segments such as medical technology, aerospace and defense, and advanced industrial applications, where products typically have longer life cycles, stringent regulatory requirements, and levels of complexity that limit competitive intensity. As a result, market participants increasingly differentiate EMS providers not by headline revenue growth, but by the quality and resilience of their business mix, given that high-reliability segments are able to sustain materially higher operating margins than consumer electronics or standardized cloud platforms.

At the same time, the evolution of artificial intelligence is transforming the data center from a relatively standardized IT environment into a highly complex industrial system.

Modern architectures are no longer based on commoditized servers, but on integrated platforms combining high-performance compute processors, specialized AI accelerators, advanced memory, ultra-high-speed networking components, and dedicated power and cooling systems. The adoption of interconnection standards such as 800G switches (referring to data transmission speeds of up to 800 gigabits per second within data centers), alongside the proliferation of multi-layer chips and advanced packaging techniques, has significantly increased the complexity of system assembly, testing, and integration. In this environment, the role of EMS providers becomes structurally more critical than in the past, as delivering a reliable, fully functional system requires industrial execution capabilities that extend well beyond basic assembly.

A critical but often underappreciated consequence of rising system complexity is the growing strain on working capital. The production of advanced AI systems requires EMS providers to pre-fund extremely expensive components, often well in advance of customer payments, while increasing levels of customization reduce inventory fungibility. At the same time, large end customers retain significant control over technical specifications, production volumes, and order timing, limiting the ability of EMS providers to offset higher capital intensity through pricing. As a result, any delay, revision, or cancellation of customer programs can quickly translate into inventory devaluation and material pressure on free cash flow. In this environment, working capital management has become one of the most important differentiators between resilient EMS operators and those whose financial performance remains structurally volatile and highly cyclical.

Taken together, the EMS sector in 2026 is characterized by a fundamental structural tension. On the one hand, it benefits from powerful secular trends and has become increasingly strategic to the functioning of the global digital economy. On the other hand, it remains an industry historically defined by modest margins, high customer concentration, and significant sensitivity to capital expenditure decisions made by a small number of large technology players. In this context, long-term value creation depends less on volume growth alone and more on the ability to control technological complexity, manage financial risk, and position the business in the most defensible segments of the value chain.

Market Positioning

Within the EMS landscape outlined above, Celestica occupies a transitional position between traditional, execution-focused EMS providers and fully integrated ODM players. Importantly, this should not be interpreted as leadership by overall EMS scale, but rather as a leading position within a higher-complexity subset of the market, hyperscaler-facing networking, platform integration, and rack-scale solutions, where engineering depth and execution reliability increasingly determine supplier selection.

Historically rooted in a classic EMS model, the company has been progressively repositioning itself toward a more design-led and system-oriented role, particularly in areas where architectural complexity, execution certainty, and speed to deployment are critical for customers. This evolution does not imply a wholesale departure from the EMS paradigm, but rather a deliberate shift toward Joint Design Manufacturing and selective ODM capabilities that allow Celestica to engage earlier in the product lifecycle and capture a greater share of the value embedded in complex infrastructure platforms.

Importantly, this repositioning has been most pronounced within Connectivity & Cloud Solutions (CCS), where hyperscaler demand increasingly favors manufacturing partners capable of contributing to platform definition rather than merely executing predefined builds. By moving closer to the design-in phase while avoiding full product ownership and brand risk, Celestica seeks to improve its economic positioning without assuming the full volatility typically associated with pure ODM models.

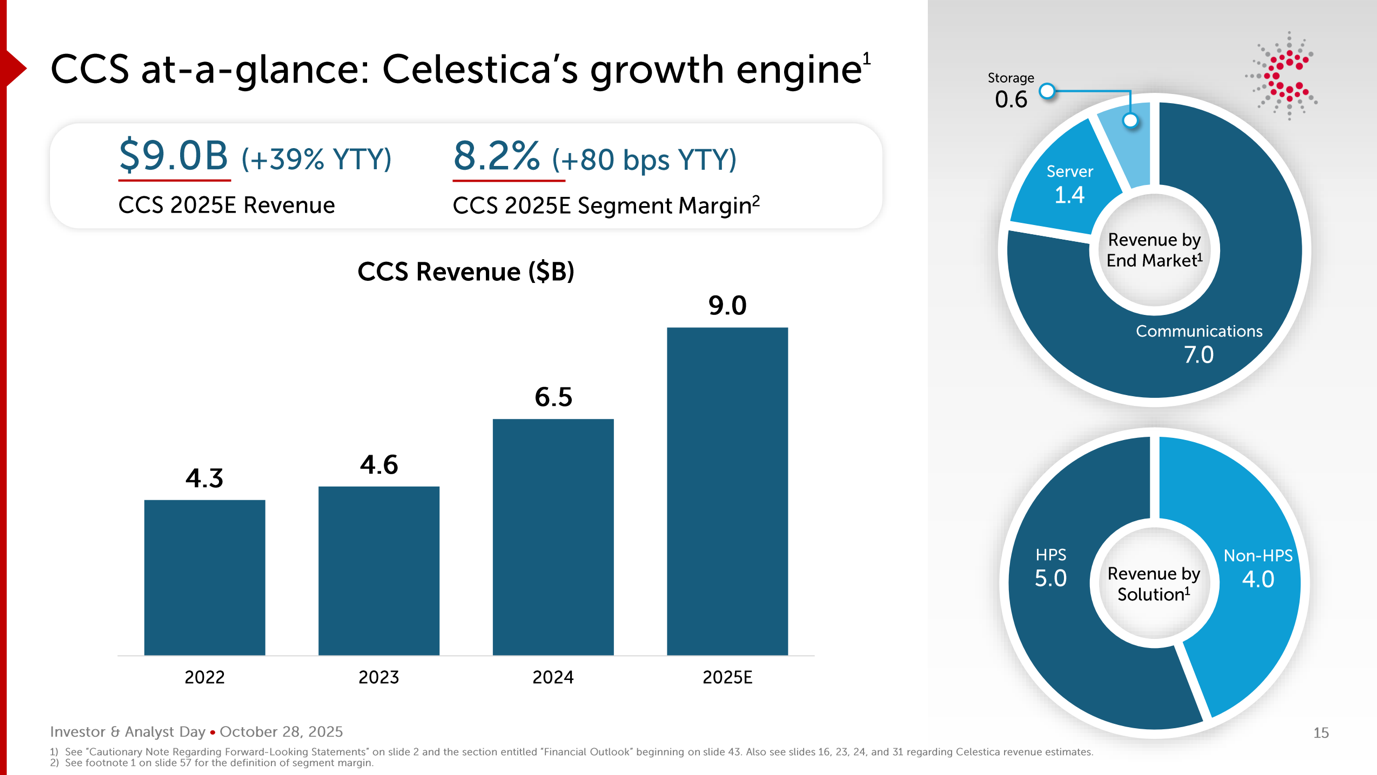

CCS represents both the primary growth engine and the strategic anchor of Celestica’s current positioning. This strategic focus is already evident in recent performance. CCS segment revenue increased by approximately 40% year-on-year in 2024, reaching $6.5 billion, driven by strong hyperscaler demand across both the Enterprise and Communications end markets. Looking ahead, management expects CCS revenue to scale further to roughly $9.0 billion in 2025E, underscoring both the momentum of AI-driven infrastructure spending and the company’s increasing reliance on this segment as the primary driver of growth.

The segment is directly exposed to hyperscaler investment in data center infrastructure, spanning compute, storage, and high-speed networking systems designed to support AI workloads. In the current cycle, demand has been driven less by incremental capacity expansion and more by urgent, large-scale deployments, where time-to-market and execution reliability often outweigh marginal pricing considerations.

Within CCS, Celestica’s role increasingly extends beyond individual server assembly toward rack-scale integration. In practical terms, value creation has shifted from the component or server level to higher layers of integration, often referred to as Level 10 and Level 11 integration. Level 10 involves the physical integration of multiple servers within a rack, while Level 11 encompasses the full integration of networking, power distribution, cooling, and, in some cases, software configuration. Celestica’s ability to deliver fully integrated, plug-and-play racks allows hyperscalers to deploy capacity more rapidly while outsourcing a significant portion of the electrical, thermal, and mechanical complexity inherent in modern AI infrastructure. This system-level role positions Celestica to capture an outsized share of hyperscaler-driven programs where time-to-market and integration reliability are prioritized over marginal cost optimization, relative to more commoditized, build-to-print EMS peers. However, CCS remains structurally characterized by high volumes, lower margins, and pronounced sensitivity to customer capital expenditure cycles. The strategic importance of CCS therefore lies not in margin expansion, but in scale, learning effects, and deepening operational integration with hyperscalers at the most complex points of their infrastructure stack.

This structural margin constraint is precisely why the strategic focus has shifted toward design-led participation and higher layers of integration: the economic upside is less about repricing standardized build work and more about increasing content, complexity, and program stickiness.

Celestica’s transition toward a more design-led role carries explicit economic objectives. By increasing participation in JDM programs, particularly within CCS, the company aims to structurally lift operating margins toward a non-IFRS range of approximately 5.5% to 6.5%, materially above the historical EMS industry average of roughly 3% to 4%. As articulated in management’s long-term non-IFRS framework, this margin ambition is intended to be driven primarily by mix and program complexity rather than an assumption of structurally improved customer bargaining power.

The company’s JDM capabilities are most visible in advanced networking and storage platforms, including 800G networking architectures and high-performance storage systems optimized for AI workloads. In these applications, early design involvement is critical to achieving signal integrity, power efficiency, and thermal stability, making the manufacturing partner’s engineering input a prerequisite rather than an optional add-on. While such capabilities do not eliminate pricing pressure, they meaningfully reduce execution risk for customers and raise switching costs at the program level.

Relative to generic EMS providers, Celestica’s differentiation is increasingly defined by its mastery of rack-scale and system-level integration rather than by pure manufacturing scale. Specifically, its edge is anchored in Level 11 (L11) rack-scale integration and liquid-to-chip cooling thermal management.

As AI workloads drive power densities higher, the integration of compute, networking, power distribution, and advanced cooling has become a binding constraint on deployment speed.

In this context, Celestica’s ability to manage 800G networking platforms, and to prepare for emerging terabit-scale switching architectures, represents a tangible technical barrier. These systems require extremely tight signal integrity tolerances, advanced testing capabilities, and precision manufacturing processes that extend well beyond traditional EMS assembly. While many peers struggle with the capital intensity and execution risk associated with such platforms, Celestica’s experience, partly derived from high-performance and high-reliability programs, allows it to compress new product introduction cycles and provide hyperscalers with a meaningful time-to-market advantage during periods of acute capacity constraints.

Working capital discipline as a competitive filter

This positioning, however, comes with elevated financial complexity. The CCS segment is inherently working-capital intensive, particularly in AI-driven cycles where high-value components such as GPUs and advanced networking modules must be procured well in advance of customer payments. The resulting pressure on the cash conversion cycle represents one of the most critical stress points in the model.

These dynamics are amplified by a high degree of customer concentration. In 2024, Celestica’s top ten customers accounted for approximately 73% of total revenue, while the CCS segment represented around 67% of consolidated revenues. Although this concentration has declined modestly compared to prior years, it continues to reinforce customer bargaining power and limits pricing flexibility, particularly in capital-intensive CCS programs.

In addition, customer order visibility remains structurally limited. Production schedules are typically committed only 30 to 90 days in advance, resulting in inherent volatility in order volumes, inventory levels, and capacity utilization. In a business model that requires significant upfront procurement of high-value components, this limited forward visibility increases execution risk and makes free cash flow inherently more volatile than reported operating earnings.

In this environment, Celestica’s ability to maintain a relatively stable cash conversion cycle despite rising volumes and system complexity becomes a key indicator of operational discipline. Effective inventory management, supplier coordination, and customer alignment increasingly differentiate resilient operators from those whose free cash flow becomes structurally volatile as volumes scale.

Peer context and structural trade-offs

Across the global EMS and ODM landscape, competitive dynamics remain structurally intense and highly fragmented. Traditional Tier-1 EMS providers continue to compete primarily on scale, cost efficiency, and global manufacturing footprint, while ODM-centric players emphasize deeper design ownership at the expense of greater balance-sheet exposure and demand volatility. At the same time, hyperscalers increasingly adopt multi-sourcing strategies, reallocating volumes across suppliers based on execution reliability, speed to deployment, supply chain resilience, and evolving geopolitical or trade considerations. As a result, revenue mix and profitability across the sector remain fluid, and even differentiated operators remain structurally exposed to re-bid risk and shifts in customer sourcing strategies.

Within this competitive environment, Celestica does not position itself as the largest EMS provider by revenue, nor as a fully integrated ODM with direct end-market exposure. Instead, its differentiation emerges from selective leadership in the most performance-critical and technologically complex segments of the data center infrastructure stack, where early design participation, manufacturing execution, and system-level integration converge. This hybrid EMS/JDM positioning allows Celestica to remain deeply embedded at points of highest architectural complexity, while avoiding the full inventory, demand, and pricing volatility typically associated with pure ODM models.

This selective form of leadership is best illustrated not at the aggregate EMS level, but within specific high-bandwidth infrastructure segments where technical execution and time-to-market are decisive. In high-bandwidth Ethernet switching, where AI-driven data center architectures depend on ultra-low latency, signal integrity, and rapid deployment cycles, manufacturing capability alone is insufficient. Success increasingly requires deep engineering involvement, tight coordination across the supply chain, and the ability to industrialize advanced designs at scale.

Celestica’s positioning in this segment provides tangible evidence of this dynamic.

Compared to competitors like Jabil, Foxconn, and Flex, Celestica stands out as a more vertically integrated player, offering a complete end-to-end service model. This includes hardware design, proprietary HPS platform development, global geographical coverage, and advanced engineering. This broad range of services makes Celestica the preferred choice for hyperscalers and high-demand customers. Additionally, Celestica’s involvement in partnerships with Meta and OpenAI in next-generation 1.6T switching platforms has created strong switching barriers for customers, making it increasingly difficult for clients to change suppliers. This is also reflected in Celestica’s higher margins in the CCS segment, which are almost double those of its competitors. Furthermore, as switch complexity increases, particularly for hyperscalers, the costs associated with switches also rise, giving Celestica a clear edge due to its superior engineering and integration capabilities.

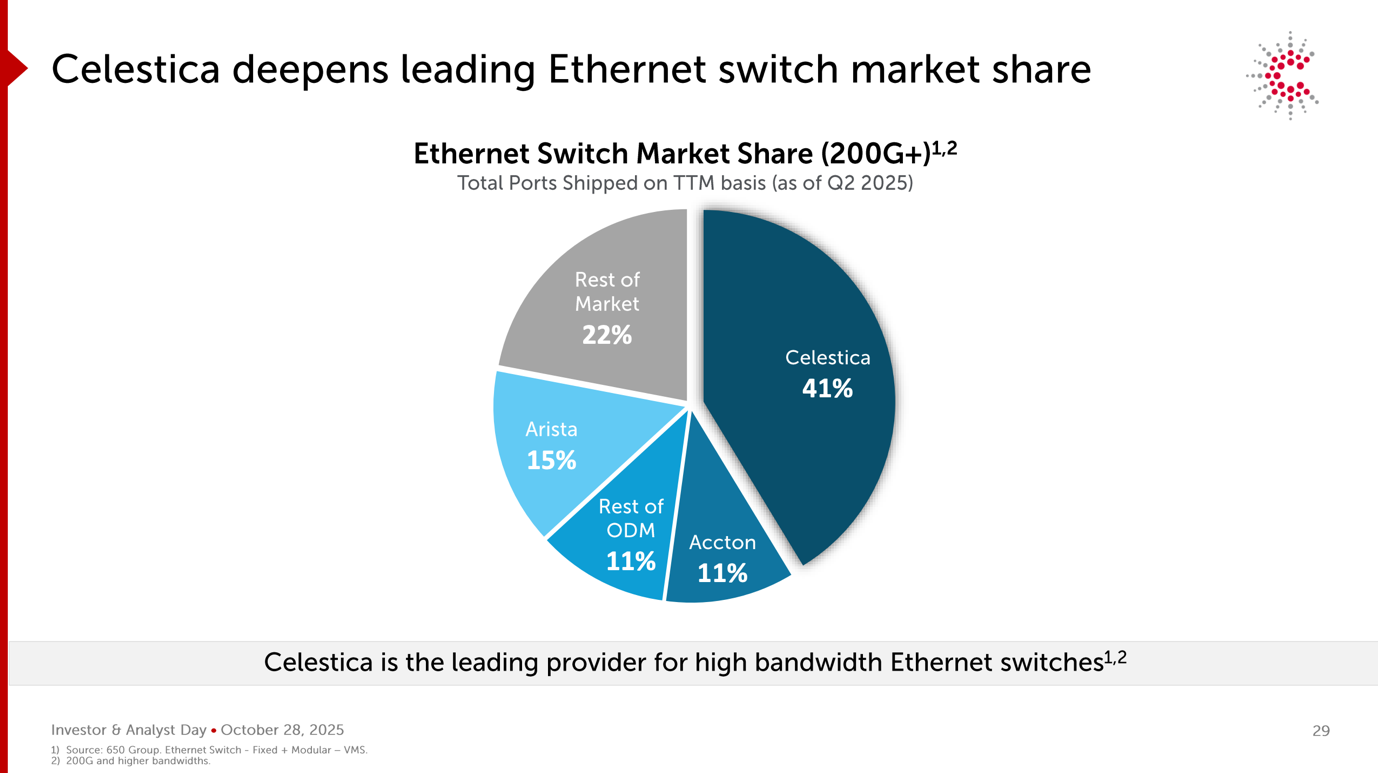

While the company reported a 41% market share in Ethernet switches above 200G on a trailing twelve-month basis as of Q2 FY2025, management noted during the Q3 FY2025 call that Celestica is on track to exceed 50% market share on a current-year run-rate basis, up from approximately 40% last year. This divergence reflects the accelerating deployment of 800G platforms and early program awards in 1.6T, which are not yet fully captured in backward-looking TTM data.

Importantly, management also disclosed that more than ten programs are already underway on 1.6T, underscoring early-cycle leadership in the next architectural transition rather than reactive participation. Together, these indicators suggest that Celestica’s advantage is not merely cyclical, but rooted in its ability to translate engineering depth into scaled deployment ahead of the broader market.

Celestica’s leading position in 200G+ Ethernet switching platforms highlights how competitive advantage in the EMS sector is increasingly defined not by overall manufacturing scale, but by control over critical bottlenecks in next-generation infrastructure deployment. This leadership reflects the company’s ability to translate early design engagement into reliable, high-volume production under compressed timelines, reinforcing its strategic relevance to hyperscalers operating under acute capacity and deployment constraints.

Recent Share Performance

Celestica delivered an exceptional equity performance in 2025, with the share price more than tripling over the year and compounding into a cumulative gain of approximately tenfold between early 2024 and the end of 2025. This rally cannot be explained by a generic re-rating of the EMS sector, which remained constrained by weak consumer electronics demand and post-pandemic normalization in traditional end markets. Instead, Celestica’s outperformance reflects a sharp divergence within the EMS/ODM landscape, driven by exposure to hyperscaler-led AI infrastructure investment.

From a sector perspective, 2025 marked a renewed acceleration in data center capital expenditures, as hyperscalers prioritized large-scale deployments of AI training and inference capacity. Unlike prior cloud investment cycles, demand was driven less by incremental capacity expansion and more by urgency, architectural complexity, and time-to-market considerations.

This shift in hyperscaler behavior was underpinned by an unprecedented acceleration in capital expenditure. Aggregate capex across the five largest hyperscalers (Amazon, Microsoft, Alphabet, Meta, and Oracle) increased from approximately $256 billion in 2024 to $443 billion in 2025, a +73% year-on-year expansion, with forecasts pointing to over $600 billion in 2026. Importantly, an estimated 75% of this spend was directly allocated to AI-related infrastructure, including GPU clusters, high-performance servers, high-bandwidth networking, and data center expansion. This magnitude of investment materially altered demand dynamics across the EMS/ODM ecosystem, disproportionately benefiting suppliers positioned at the intersection of system complexity, execution reliability, and rapid deployment.

This environment disproportionately favored manufacturing partners capable of executing high-speed networking, advanced compute, and system-level integration at scale. Celestica’s Connectivity & Cloud Solutions (CCS) segment sits directly at this intersection, benefiting from increased hyperscaler spending on AI-optimized networking platforms and server infrastructure.

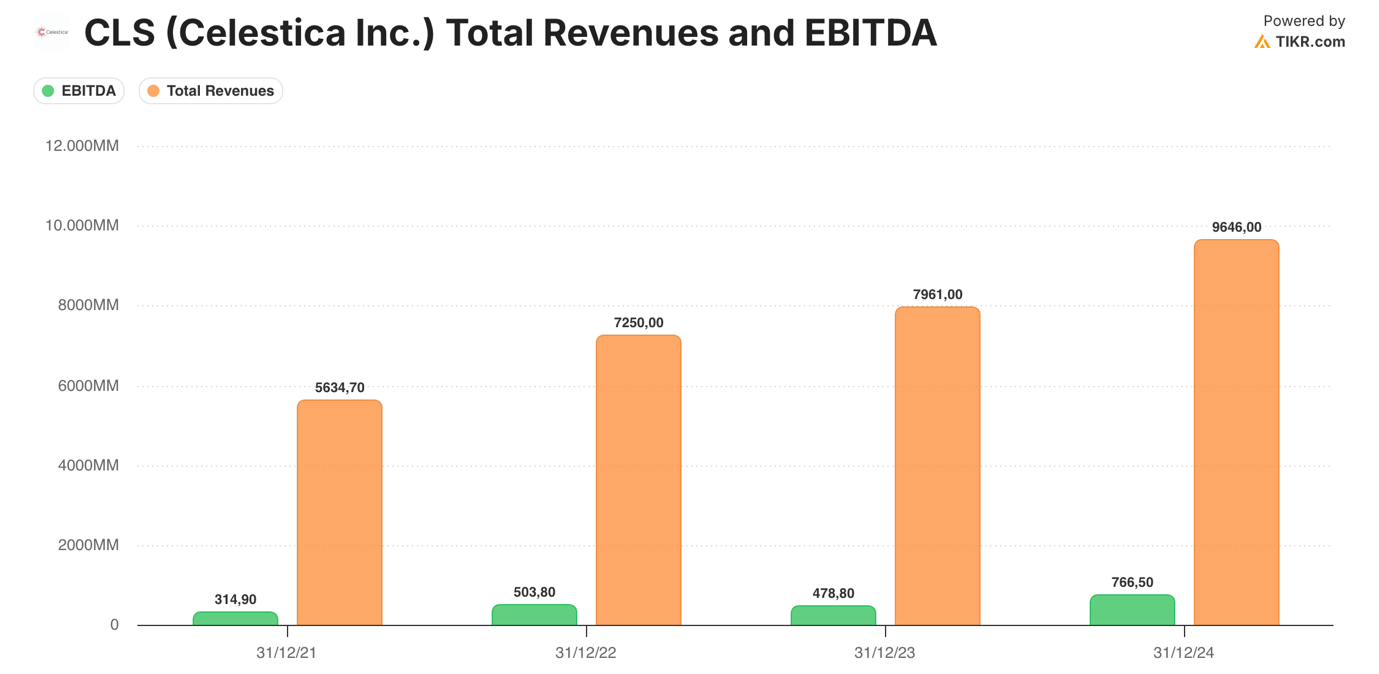

This structural tailwind translated into a material inflection in operating performance. Between 2021 and 2024, Celestica’s revenues grew from approximately CAD 5.6 billion to CAD 9.6 billion, with CCS increasingly accounting for the majority of incremental growth. In 2024 alone, CCS revenues expanded by roughly 40% YoY, driven by strong demand across both Enterprise and Communications end markets. Importantly, this growth was accompanied by improving mix quality rather than pure volume expansion, reflecting a shift toward higher-complexity programs within advanced networking and AI-related workloads.

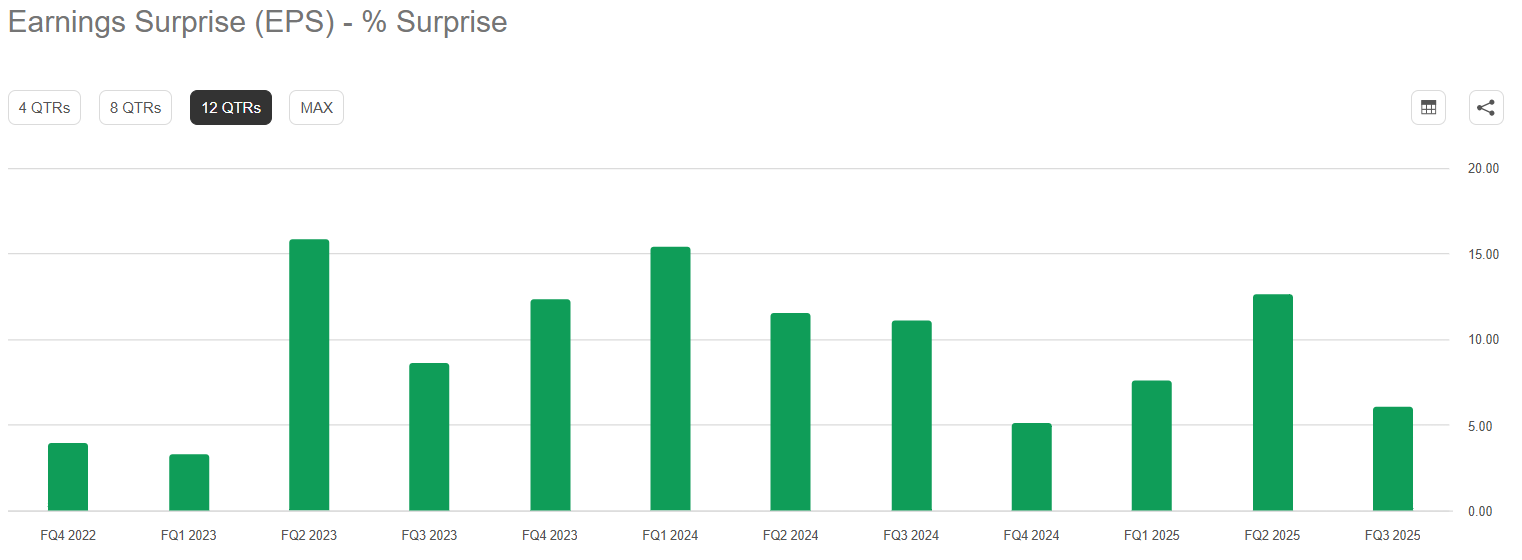

Financial execution reinforced the equity narrative throughout 2025. Reported results consistently exceeded market expectations, supported by operating leverage, scale efficiencies, and disciplined cost control. Margins expanded meaningfully as CCS volumes scaled, while free cash flow generation improved despite the working-capital intensity of AI-driven programs. Free cash flow increased materially between 2022 and 2024, reflecting both higher earnings power and improved balance sheet discipline, including deleveraging and tighter capital allocation.

As a result, investor perception shifted decisively. Celestica began to be valued less as a cyclical, low-margin EMS provider and more as a structurally advantaged enabler of AI infrastructure deployment. The equity rally in 2025 therefore reflects not only strong reported growth, but a reassessment of the company’s long-term earnings durability, relevance within the AI capex cycle, and ability to capture a disproportionate share of hyperscaler-driven demand relative to traditional EMS peers.

Recent Financial Performance and Operating Inflection

The structural acceleration in hyperscaler-led AI infrastructure spending translated directly into a marked inflection in Celestica’s financial performance throughout 2025. In the third quarter, revenue reached $3.19 billion, up 28% YoY and above the high end of management guidance, reflecting stronger-than-anticipated demand across communications and enterprise programs. Growth was overwhelmingly driven by the Connectivity & Cloud Solutions segment, where revenues increased 43% YoY to $2.41 billion, underscoring the company’s growing exposure to high-speed networking, AI-optimized server platforms, and system-level integration for hyperscale customers. The growth was driven by very strong demand in data center networking, primarily for ramping 800G switch programs across our largest hyperscaler customers, complemented by solid demand in our optical programs.

Importantly, this top-line acceleration was accompanied by a meaningful expansion in profitability, signaling a shift in mix quality rather than pure volume-driven growth. Adjusted operating margin reached 7.6% in Q3 2025, a new company high, compared to 6.8% in the prior-year period, driven by operating leverage, scale efficiencies, and a higher proportion of complex, higher-margin CCS programs. Adjusted EPS rose 52% year-on-year to $1.58, significantly outperforming expectations and highlighting the earnings sensitivity embedded in the business model as AI-related volumes scale.

At the segment level, CCS margins expanded to 8.3%, reflecting both favorable program mix and improved execution. A key driver was the Hardware Platform Solutions (HPS) business, which generated $1.4 billion in revenue (up 79% YoY), now accounting for 44% of total company revenue. Management attributed this surge to accelerating volumes in ramping 800G switch programs for major hyperscalers.

This robust growth in networking more than offset the 24% decline in the Enterprise end market. Rather than a loss of market relevance, this contraction reflects a pivotal shift in hyperscaler CapEx allocation: budget is being redirected away from legacy general-purpose compute and storage toward specialized AI/ML infrastructure. This transition, evidenced by the ramping of new compute programs, confirms that Celestica is successfully capturing the higher-value portion of the evolving data center stack.

By contrast, the ATS segment declined 4%, falling below guidance due to deliberate portfolio reshaping within the A&D (Aerospace & Defense) business. Collectively, these dynamics reinforce the view that Celestica’s performance is structurally tied to this massive reallocation of capital toward AI infrastructure, specifically high-complexity HPS solutions, rather than a broad-based cyclical rebound across all end markets.

Free cash flow generation also improved meaningfully despite the working-capital intensity associated with rapid growth. For the first nine months of 2025, non-GAAP free cash flow reached $302 million, supporting balance sheet strengthening and deleveraging. Reflecting this momentum, management raised full-year 2025 guidance to $12.2 billion of revenue and $5.90 of adjusted EPS, and introduced a 2026 outlook calling for $16.0 billion of revenue and $8.20 of adjusted EPS, implying continued operating leverage as AI-driven demand persists.

Financial Risk

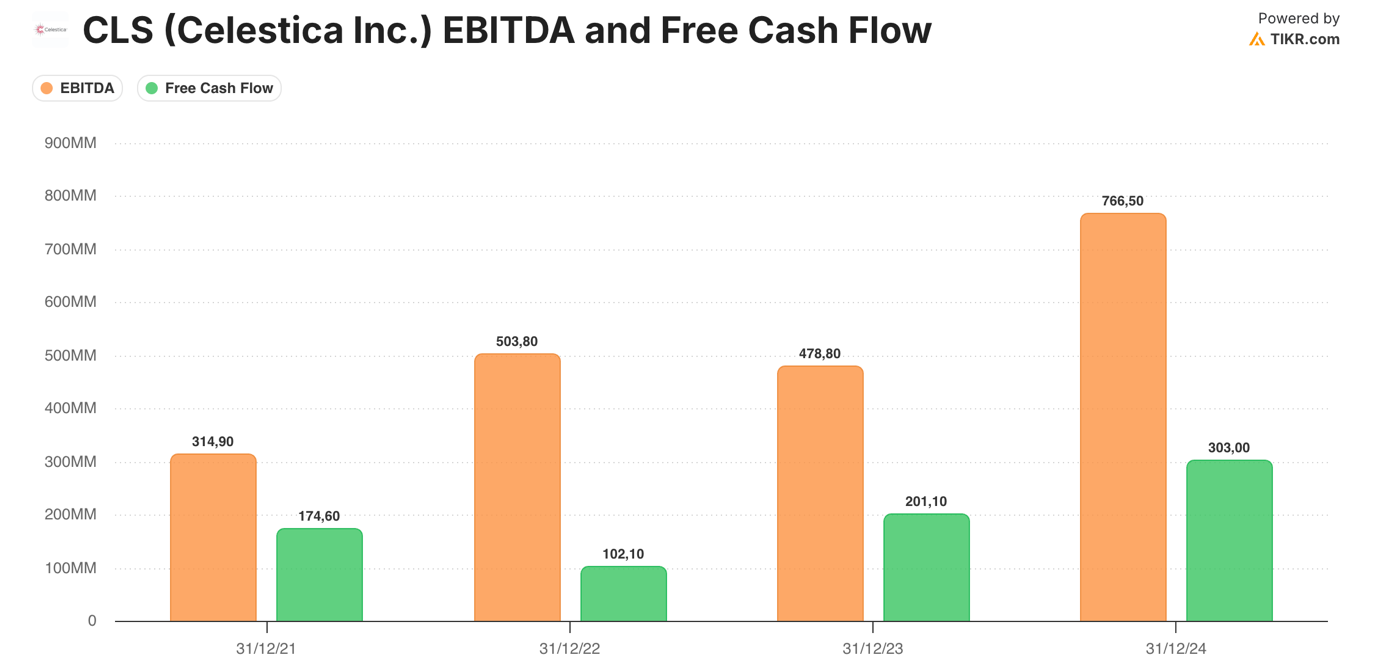

From a balance sheet perspective, Celestica operates today with a financial risk profile that appears well controlled and progressively improving, despite the capital-intensive nature of its AI-driven growth. As of FY2024, the company generated approximately CAD 766 million of EBITDA on revenues of CAD 9.6 billion, providing a solid earnings base against which to assess leverage and cash flow sustainability.

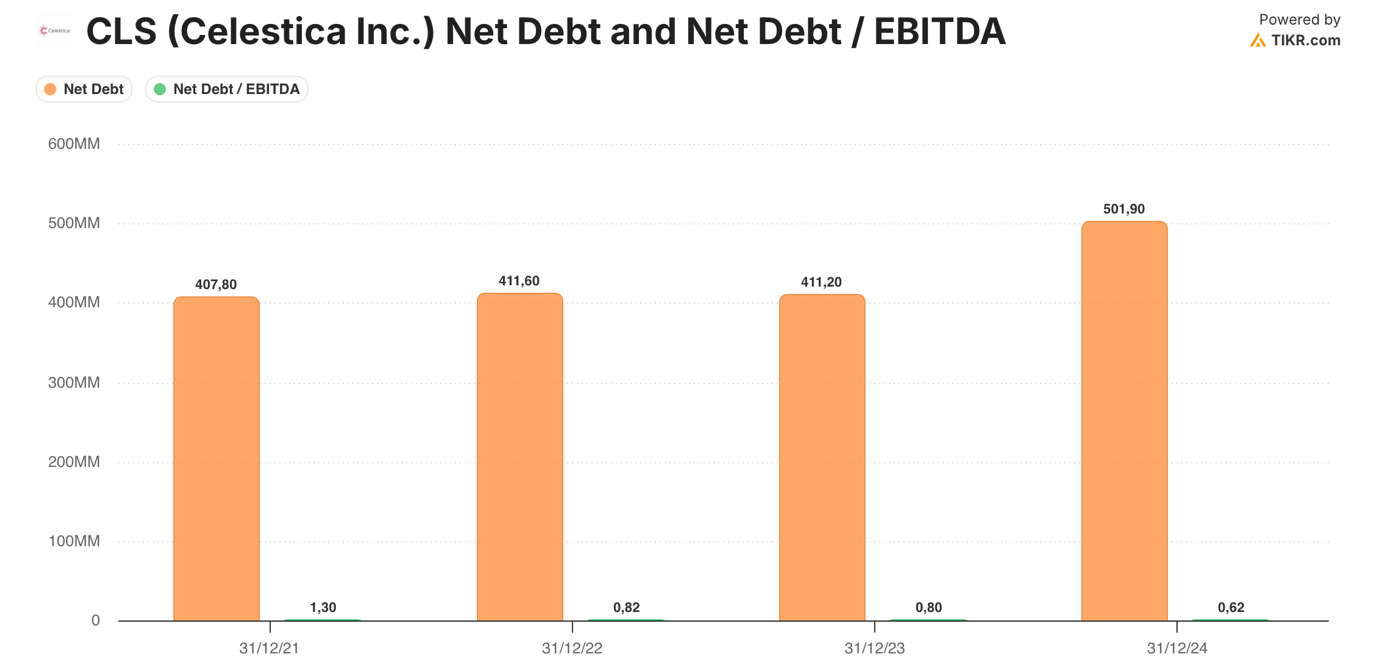

Net debt stood at approximately CAD 502 million at year-end 2024, implying a Net Debt / EBITDA ratio of 0.6x, down materially from 1.3x in 2021 and 0.8x in 2022–2023. This steady deleveraging trend reflects both EBITDA expansion and disciplined capital allocation, rather than balance sheet optimization driven by asset sales or one-off items.

Importantly, this balance sheet strength is underpinned by consistent free cash flow generation. Over the 2021–2024 period, Celestica generated cumulative free cash flow of approximately CAD 780 million, with annual FCF rising from CAD 175 million in 2021 to CAD 303 million in 2024. This translates into an average FCF conversion of roughly 40–45% of EBITDA over the period, improving meaningfully in the last two years as scale efficiencies, margin expansion, and tighter working capital management partially offset the structurally higher capital intensity of AI-related programs.

Cash flow deployment has been balanced but clearly shareholder- and balance-sheet-oriented. Between 2021 and 2024, Celestica repaid over CAD 4.0 billion of gross debt, as reflected in cumulative debt repayments reported in the cash flow statement, while simultaneously returning capital to shareholders through opportunistic share repurchases, which accelerated in 2024. Importantly, this deleveraging was achieved alongside a growing EBITDA base, resulting in a structurally lower leverage profile rather than a temporary balance sheet improvement. With leverage declining and free cash flow generation becoming increasingly predictable, management gained greater flexibility in capital allocation, enabling a more proactive return of capital to shareholders without undermining balance sheet resilience.

Notably, these buybacks were executed without compromising leverage metrics, highlighting management’s confidence in the durability of free cash flow generation even as capex requirements increased to support AI-optimized infrastructure and advanced networking programs.

Overall, Celestica’s financial risk profile is characterized by low leverage, improving interest coverage, and resilient free cash flow generation. While working capital absorption and elevated capex remain structural features of the business model, particularly in the context of hyperscaler-driven AI deployments, the company’s strong EBITDA growth and disciplined capital allocation provide a substantial buffer against cyclical volatility. As a result, financial risk appears contained and well aligned with the company’s current growth trajectory, rather than acting as a constraint on strategic execution.

Investment Thesis

The investment thesis for Celestica rests on the view that the market is underestimating a structural re-acceleration in the Connectivity & Cloud Solutions segment, which today represents roughly 75–80% of group revenues and is directly exposed to AI-driven data center and ultra-high-speed networking infrastructure. Following the strong growth experienced in 2024, consensus expectations now imply a deceleration, while management commentary and underlying industry dynamics point instead to sustained, and potentially accelerating, growth through 2026 and into 2027.

At the core of the thesis is the technological transition from 800G to 1.6T networking, expected to begin toward the end of 2026 and scale meaningfully in 2027. This is not a standard product refresh, but a step-change in network architecture required to support rapidly rising AI workloads.

Margins are expected to remain stable in the short term. However, the strong growth expected in the CCS segment, alongside the shift towards 1.6T switching, should provide room for margin expansion, potentially exceeding current expectations.

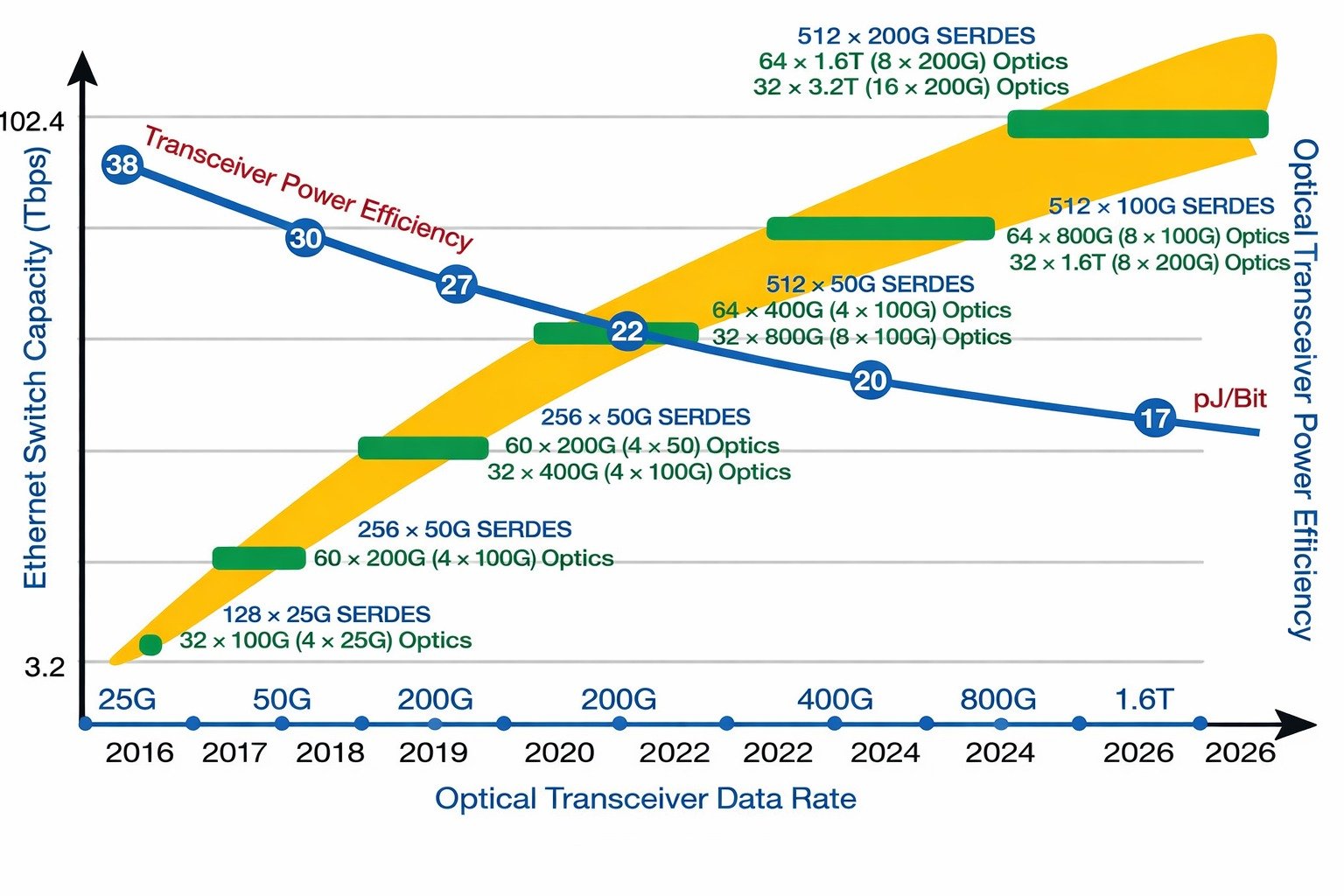

This architectural step-change is evident in the non-linear scaling of switch capacity, SERDES density, optical complexity, and power efficiency required to move from 800G to 1.6T systems, materially increasing integration challenges and barriers to entry.

*The chart illustrates how the evolution from 100G to 400G, 800G and ultimately 1.6T Ethernet is not a simple increase in speed, but a structural transformation of data-center networking architecture. As optical transceiver data rates rise, overall switch capacity scales exponentially, driven by the need to interconnect ever-denser AI compute clusters. At the same time, the number of SERDES lanes (high-speed serializer/deserializer interfaces that convert parallel data into serial streams and vice versa for chip-to-chip and chip-to-optics communication), optical channels and power density per system increases sharply, making thermal management and energy efficiency critical constraints. While energy consumed per bit continues to decline, this improvement is only achievable through far more complex system design, advanced cooling solutions and deep integration between compute, networking, optics and power delivery. In practical terms, the transition to 1.6T represents a step-change in system complexity rather than a routine product refresh, favoring suppliers with strong co-design capabilities, execution know-how and the ability to deliver highly integrated, thermally optimized platforms at scale.

Industry estimates suggest demand for 1.6T optical modules could increase from roughly 1 million units in 2025 to around 5 million units in 2026, with a substantial share driven by Google’s TPU-based rack deployments. Importantly, despite 800G modules growing over 100% in 2025, Celestica’s CCS revenues increased only 20–30% over the same period, highlighting that the revenue impact of the current upgrade cycle has not yet fully translated through pricing and mix.

From an economic standpoint, the shift to 1.6T should result in materially higher average selling prices, potentially 60–70% above 800G, while still incentivizing customers to migrate. Although some cannibalization of 800G volumes is inevitable, it is unlikely to exceed 20% of revenues. Under a scenario where 1.6T optical module volumes grow even 200%, CCS revenues could plausibly increase by 60–70%, well above current consensus assumptions. This view is consistent with management’s implied guidance: consolidated revenue guidance of approximately $3.45 billion for 4Q FY2025, assuming a largely flat ATS contribution of around $800 million, implies CCS revenues of roughly $2.7 billion, or more than 50% year-over-year growth. In addition, 1Q FY2025 represents a relatively weak comparison base, suggesting CCS growth could again approach 50% in 1Q FY2026.

Margin dynamics further strengthen the thesis. CCS carries structurally higher profitability than the rest of the portfolio, and as it approaches 80% of total revenues, operating leverage should drive EBIT margins above the currently guided 7.6%, which appears conservative and broadly in line with recent quarters.

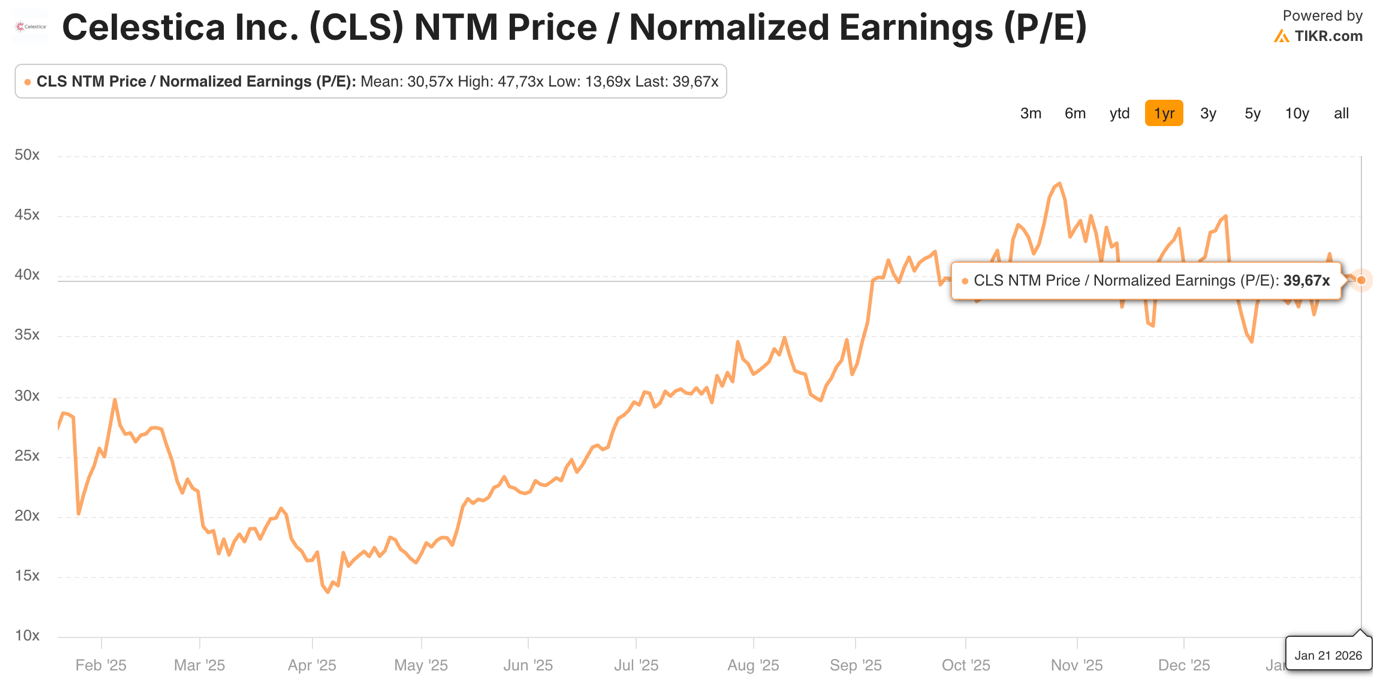

If CCS growth accelerates while margins continue to expand, it becomes increasingly difficult to justify a compression in valuation multiples. In this context, a decline in the forward P/E from 48x to 39x, as implied by consensus, appears inconsistent with the underlying earnings trajectory. While an entry point closer to 35x would be ideal, the current valuation already offers asymmetric upside should earnings revisions materialize.

Celestica’s competitive positioning further differentiates the story. The company has already completed a structural transformation from a traditional EMS provider to a co-design and joint development partner, embedding itself deeply into customer architectures. This model increases switching costs, improves revenue visibility, and enhances backlog quality.

As a result, Celestica is well positioned to be among the limited number of global suppliers capable of supporting meaningful volumes at 1.6T, a scarcity value that could justify a valuation premium for technological leadership. While software-oriented players such as Arista Networks should also benefit from the 1.6T upgrade cycle through new switch deployments and software layers, Celestica operates at a more constrained and critical point of the supply chain, where execution risk and technological barriers are highest.

The investment case for Celestica combines high AI exposure, a potential re-acceleration in CCS growth, operating leverage on margins, and meaningful re-rating optionality, balanced against higher dependence on the data center investment cycle. If the market continues to underestimate the scale and economics of the 1.6T transition, the risk-reward profile over the next 12–24 months remains compelling.

Looking ahead, the investment case is further reinforced by a combination of accelerating end-market demand, expanding addressable market, and operating leverage that remains underappreciated by consensus. The total addressable market for high-bandwidth Ethernet networking is now expected to reach approximately $50 billion by 2029, with the 800G and above segments growing at an estimated 54% CAGR, driven by hyperscaler upgrade cycles and the rapid scaling of AI workloads. Importantly, management commentary suggests that the adoption of scale-up Ethernet architectures represents a meaningful incremental opportunity rather than a zero-sum shift within the existing Ethernet market, effectively expanding the TAM rather than merely redistributing spend.

Within this context, Celestica’s enterprise exposure, including AI/ML compute and storage, provides an additional layer of upside. Portfolio revenues in this segment are expected to reach approximately $2 billion in 2025 and to grow meaningfully in 2026, surpassing prior peak levels from 2024 as next-generation AI/ML compute programs ramp.

Combined with the continued strength of CCS, this supports management’s expectation that revenues in 2026 will more than double relative to 2022, while adjusted EPS could increase by more than four times over the same period, driven by sustained non-GAAP operating margin expansion. Notably, management continues to signal further operating leverage beyond 2026, suggesting that margin normalization is not yet complete.

While official guidance remains deliberately conservative, implying roughly 40% CCS growth in 2026 following similar growth in 2024 and 2025, management has explicitly acknowledged multiple upside vectors that could push growth beyond this level. These include incremental digital-native wins and additional program ramps with some of the company’s largest hyperscaler customers, with visibility already extending into 2027. As such, consensus assumptions of decelerating growth appear increasingly misaligned with both underlying demand signals and management’s own qualitative outlook.

Under a base case scenario that assumes continued CCS revenue acceleration, incremental margin expansion, and a normalization of valuation multiples, the upside potential becomes asymmetric. Celestica’s current quarterly EPS growth of approximately $0.20 suggests that consensus expectations may be overly conservative.

Assuming a continued quarterly EPS increase of $0.30 over the next 12 months, adjusted EPS could reach approximately $9 in FY2026, reflecting an annual growth rate of approximately 60%. Thanks to this renewed acceleration, particularly in the CCS segment, we see room for a potential multiple appraisal, with forward P/E multiple expected to increase towards 45-50x (vs. current 43x). Based on this range, we estimate Celestica’s implied intrinsic value to be around $425 USD per share. This estimate also translates to an equivalent value of approximately CAD 575 per share, considering Celestica’s dual listing in both USD and CAD, offering potential upside of approximately 25% from current levels. In this framework, valuation expansion is not predicated on multiple exuberance, but rather on earnings durability, structural growth, and increasing confidence in Celestica’s role as a critical enabler of next-generation AI infrastructure.

While the upcoming earnings report may induce some short-term volatility in the stock price, this does not alter the medium-term investment thesis. We remain confident that the expected growth in CCS and the technological transition to 1.6T will continue to drive long-term value, even amidst near-term market fluctuations.

All opinions and views mentioned in this report constitute our judgments as of the date of writing and are subject to change at any time. The information contained in this material is not intended to be used as the primary basis for investment decisions and should not be construed as advice that meets the particular investment needs of an individual investor. Please note that investing involves risk, including loss of principal, and past performance may not be indicative of future results. Luminaria Research, its members, officers, directors, and employees expressly disclaim any liability for actions taken based on all or any part of the information contained in this writing.