Ticker: TSM

Price: 292 USD

Target: 420 USD

Closed: 420 USD

Company overview

Taiwan Semiconductor Manufacturing Company Limited, is a Taiwanese corporation founded in 1987 and headquartered in Hsinchu City. It is recognized as the global leader in semiconductor manufacturing.

The company operates as a pure-play foundry, providing fabrication, packaging, testing, and sales services for integrated circuits and other semiconductor devices on behalf of global clients across Taiwan, China, Europe, the Middle East, Africa, Japan, and the United States.

The foundry market

Over time, the “fabless” business model has become the global standard in the semiconductor industry. In this model, Western companies (primarily based in Silicon Valley) focus on chip design, while Eastern companies (predominantly foundries located in Asia, featuring lower production costs) are responsible for the physical manufacturing of these chips.

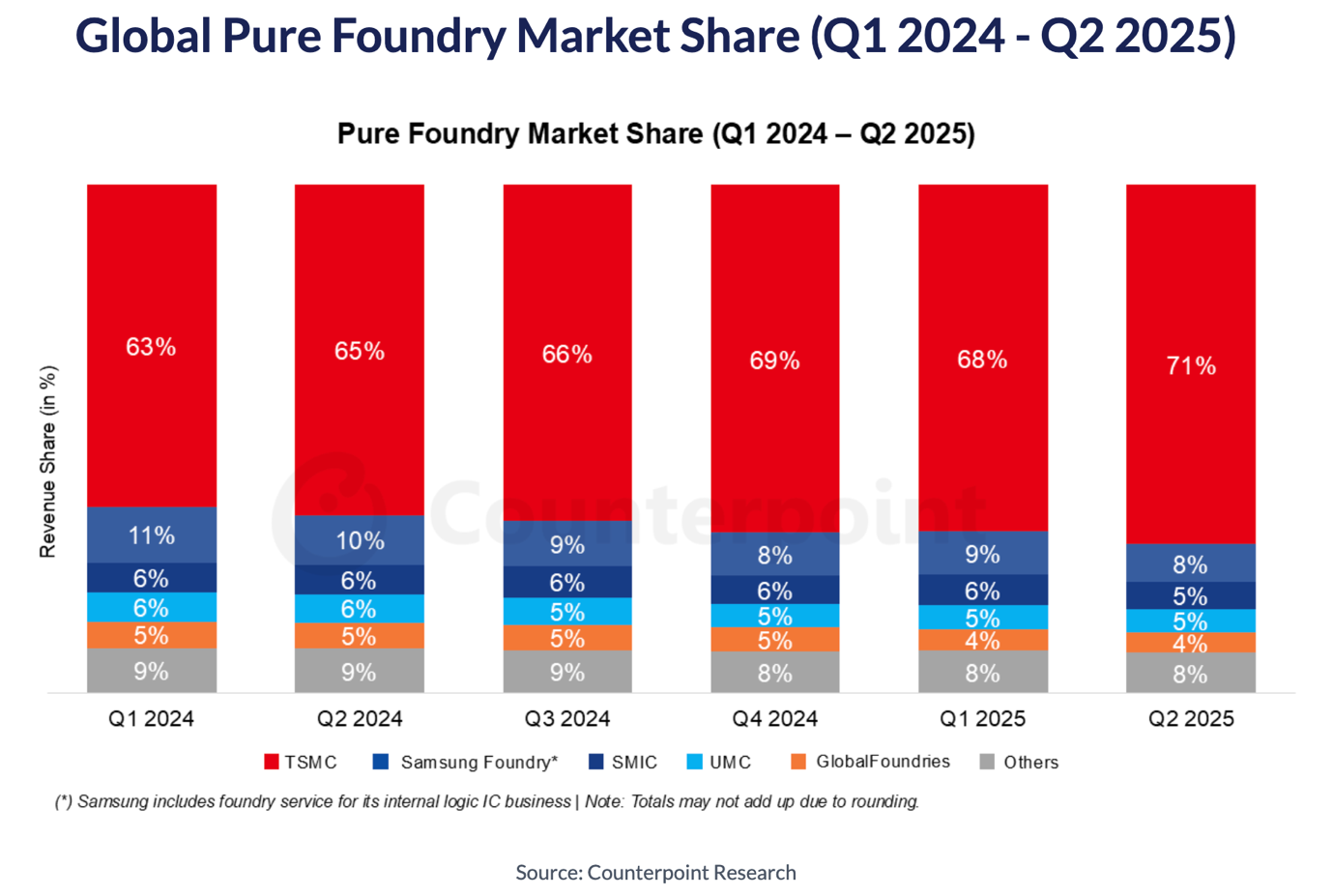

TSMC holds a 71% market share in the pure foundry segment, up from 63% in the first quarter of 2024. This sharp increase highlights the company’s extraordinary growth trajectory and its dominant position as the world’s leading third-party semiconductor manufacturer.

The industry in which TSMC operates is characterized by a “winner-takes-all” dynamic, marked by significant consolidation and the dominance of a few major players. This is driven by substantial economies of scale (where increased production volumes lead to lower unit costs) and strong customer lock-in (as switching foundries is both costly and time-consuming once a chip design is tailored to a specific manufacturer).

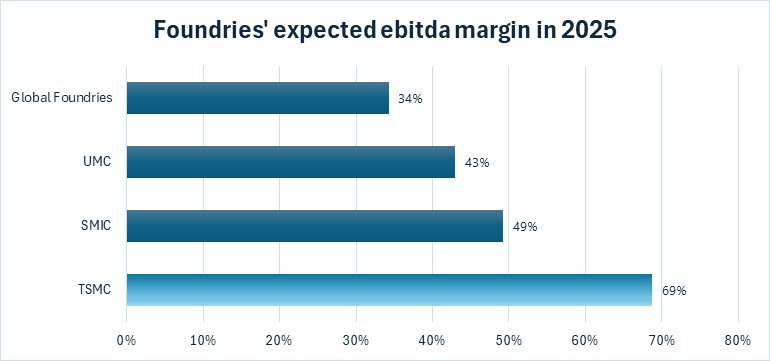

As a result, larger players are able to achieve progressively higher profit margins and advance technologically at a much faster pace than their smaller competitors.

As a matter of fact, TSMC’s leadership stems from unparalleled technological know-how in chip miniaturization, having now reached the 2-nanometer threshold.

The company’s manufacturing process is regarded as an absolute benchmark of excellence within the industry, thanks to its engineering precision and exceptionally high production yield rate, which allows it to far outperform its main competitor, Samsung Foundry, still struggling with lower yields on 3 nm chips.

Confirming this technological dominance, TSMC has already begun collaborating with AMD to produce the first 2 nm chips and plans to introduce sub-2 nm nodes by 2026, further strengthening its competitive edge in advanced semiconductor manufacturing.

Recent share performance drivers

The stock has delivered an outstanding performance since the beginning of the year, despite a challenging macroeconomic and geopolitical backdrop, rising 45% year-to-date after an already remarkable +98% in 2024. This result significantly outpaces the S&P 500, which gained 17% over the same period, underscoring how TSMC has been an amplified beneficiary of sector dynamics driven by artificial intelligence.

The strong demand for artificial intelligence is driving TSMC to gradually shift its production capacity toward lines dedicated to the most advanced chips.

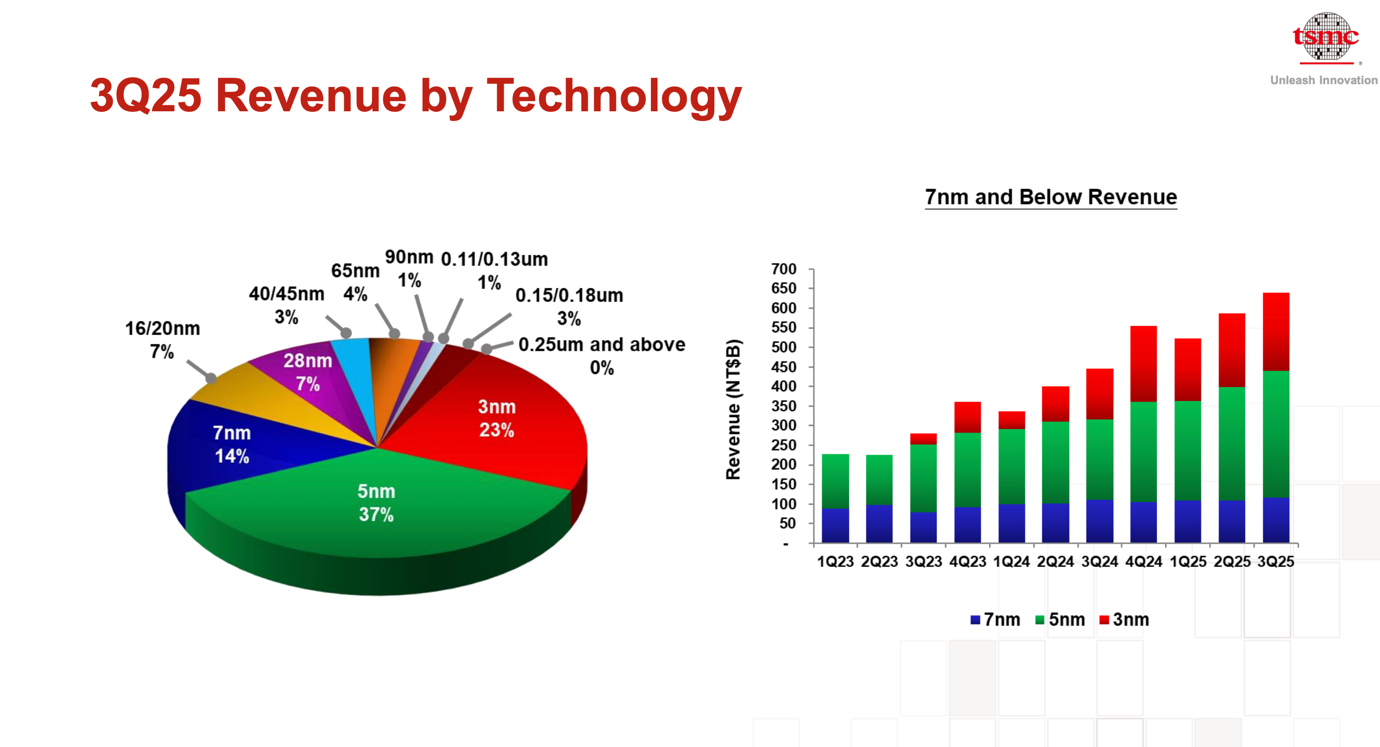

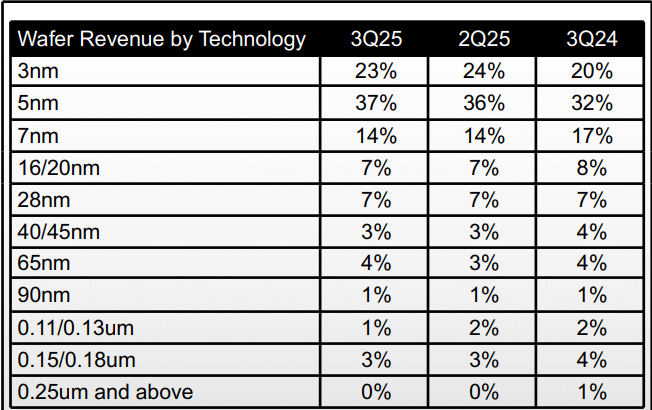

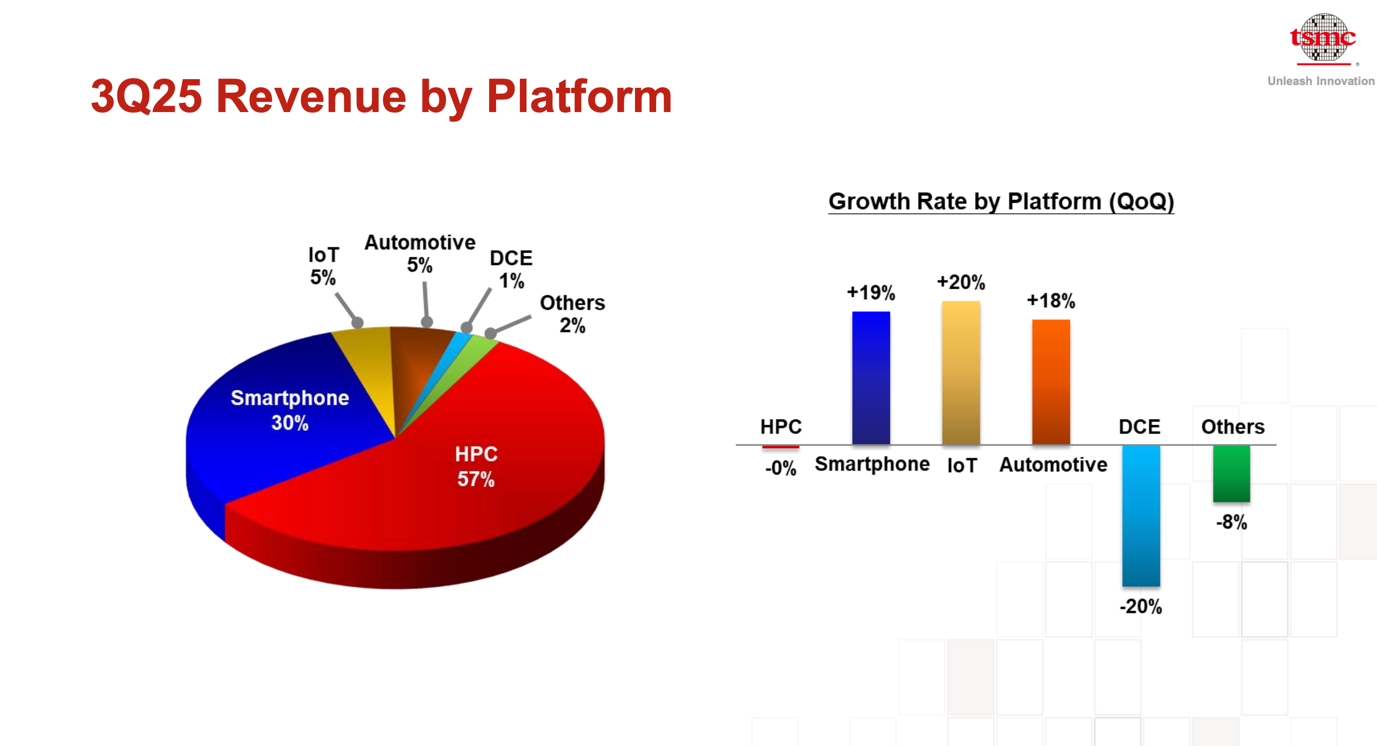

Year after year, the share of output from 5 nm and 3 nm nodes, the most sophisticated currently in mass production, continues to rise. These chips are designed to handle extremely heavy workloads and are primarily used in AI and High-Performance Computing (HPC) applications.

It is therefore reasonable to expect that the share of revenue generated by these advanced nodes will keep expanding, given that they already account for roughly 60% of total sales, supported by massive investments from Big Tech companies and governments in AI-related infrastructure.

Although TSMC is inherently a cyclical business by virtue of being a foundry, it is currently experiencing a phase of apparent acyclicality: the extraordinary demand for advanced chips is placing the company in a structurally expanding position, temporarily able to transcend the typical dynamics of the industrial cycle.

It is indeed evident that TSMC is progressively reducing the share of its production dedicated to 7-nanometer chips, which has declined by roughly three percentage points over the past year, in favor of more advanced nodes.

During the same period, the share of 5-nanometer chip production increased by about five percentage points, while 3-nanometer output grew by three points, confirming the company’s steady shift in manufacturing capacity toward more sophisticated, high–value-added technologies.

As further evidence of this trend, the High-Performance Computing (HPC) segment now accounts for nearly 60% of TSMC’s total revenue, highlighting the growing importance of chips designed for artificial intelligence and data center applications. In contrast, segments that rely on larger nodes and less advanced technologies (with lower profitability), such as automotive, represent a much smaller share, contributing roughly 5% of total sales.

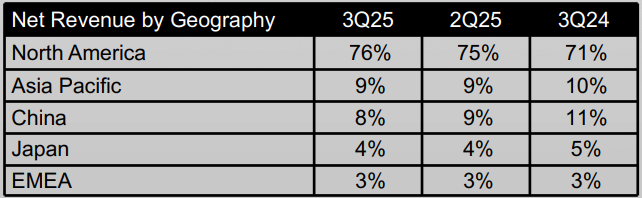

TSMC’s growing geographic dependence on North America continues to strengthen. Although many analysts view this as a potential risk, we believe that, at least in the short to medium term (12–18 months), as long as Big Tech companies maintain high levels of capital expenditure, the company can continue to sustain strong growth rates.

An additional source of strength lies in the fact that investments are no longer driven solely by the private sector: governments are also allocating significant resources toward building the infrastructure required to support artificial intelligence. We are, in fact, at an inflection point in chip production driven by AI revolution, and TSMC stands at its core, contributing to the creation of the technological foundations upon which the economy of the coming years will be built.

Current financial performance

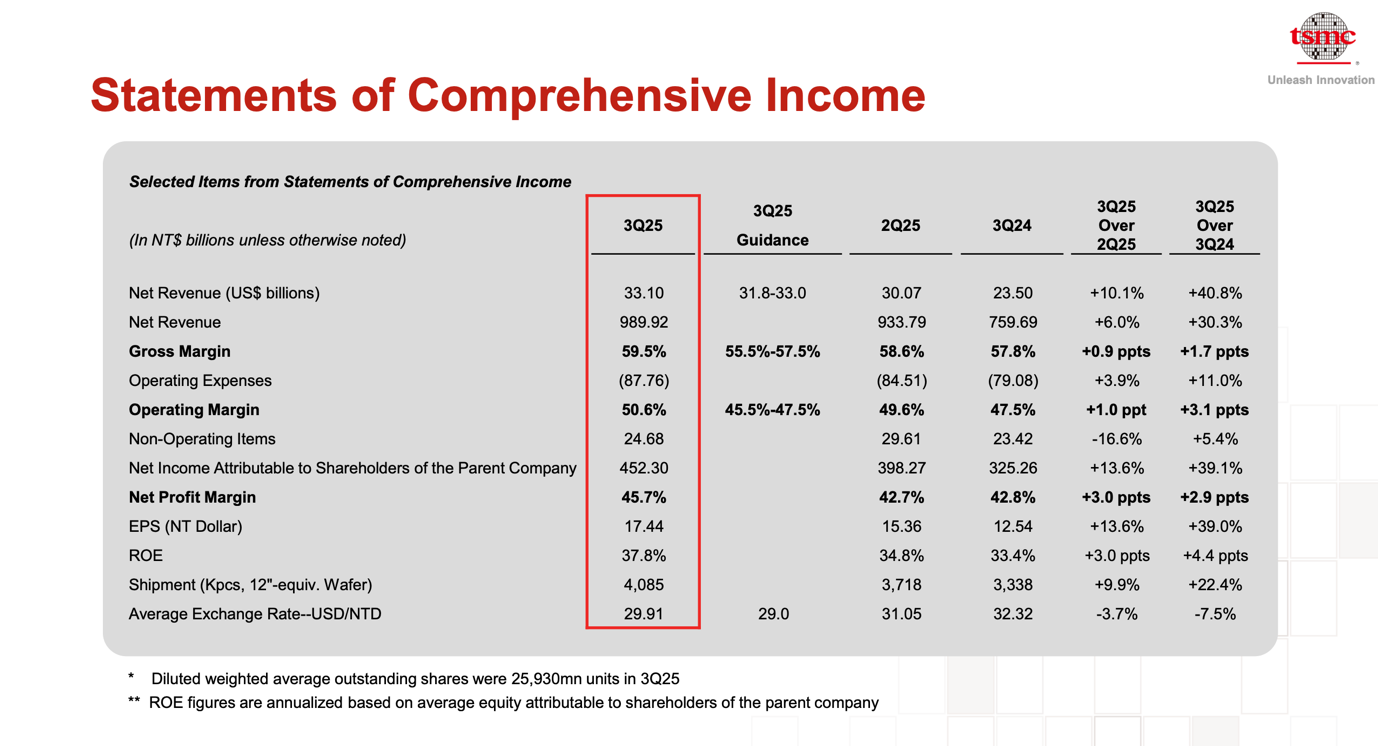

Confirming its exceptionally solid financial profile, TSMC reported outstanding quarterly results. In the third quarter of 2025, the company posted revenue of $33.1 billion, up roughly 40% year over year compared to the third quarter of 2024, far exceeding market expectations despite an already high comparison base.

Particularly noteworthy is the continued expansion of operating margins, an achievement far from trivial for a manufacturing company like TSMC, which operates as a pure-play foundry rather than a software firm.

The company exceeded its own guidance across all major profitability metrics, reporting a gross margin of 59.5%, an operating margin of 50.6%, and a net profit margin of 45.7%.

These results underscore TSMC’s ability to maintain high operational efficiency even amid rising costs, including those associated with the launch of new facilities, such as the plant in Arizona, and higher electricity prices in Taiwan.

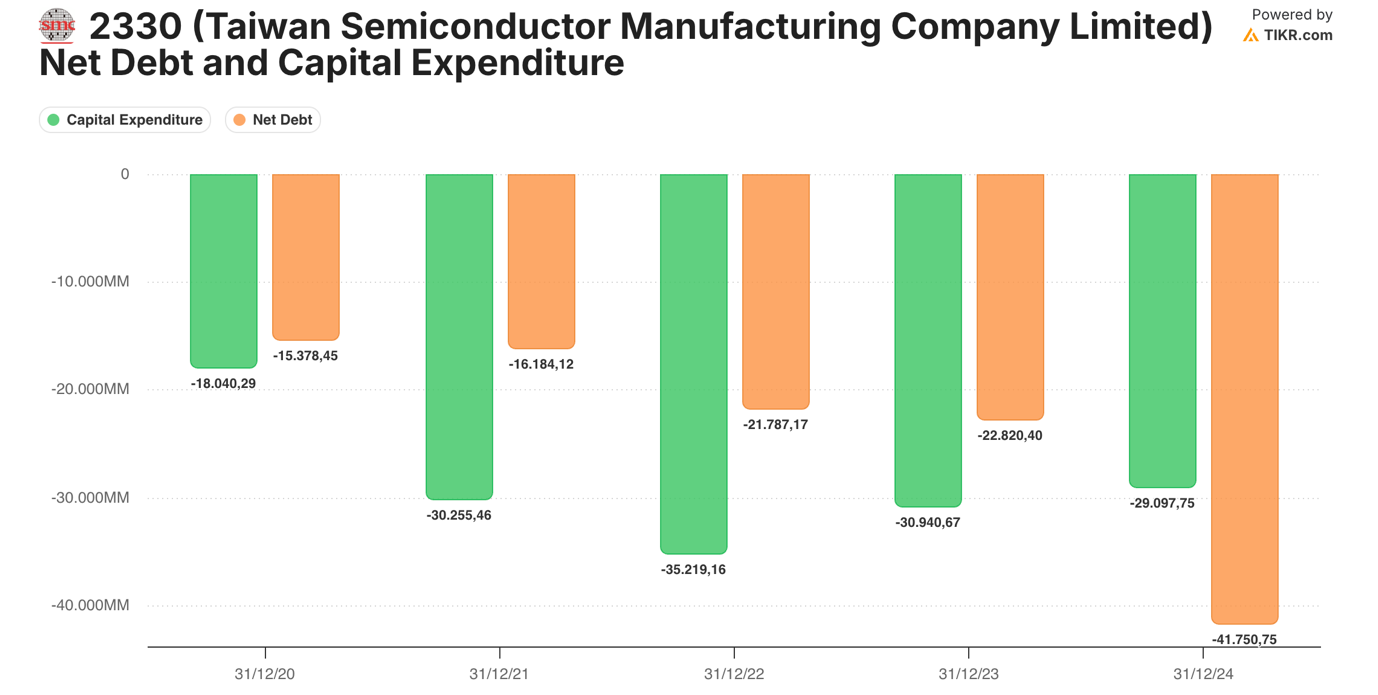

TSMC’s excellent financial management is also clearly reflected in the evolution of its negative net debt position (or net cash position), increased by more than twofold in absolute terms in the last 4 years, from approximately -$15 billion to -$41.75 billion, despite substantial capital investments during the same period. As illustrated by the chart, capital expenditures have increased significantly, reflecting the company’s aggressive expansion strategy.

Between 2022 and 2024, TSMC maintained an average cash conversion rate of 33%, demonstrating a remarkable ability to generate operating cash flow while continuing to invest heavily in future growth. The company’s cash flows are allocated both to shareholder returns through dividends and, above all, to reinforcing its market share through sustained growth and consistent reinvestment of profits into strategic initiatives.

Investment thesis

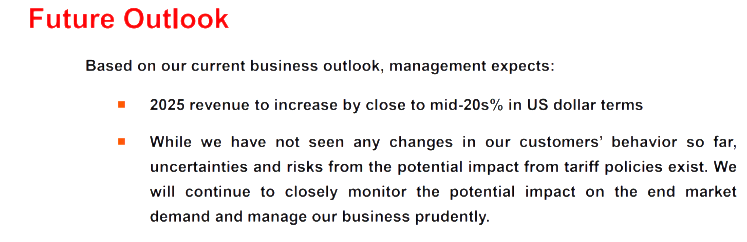

At the beginning of the year, TSMC guided for a 2025 revenue growth close to mid-20s%, while it will eventually grow by 35% in 2025, in a sign of both a strong demand and a very prudent managerial approach.

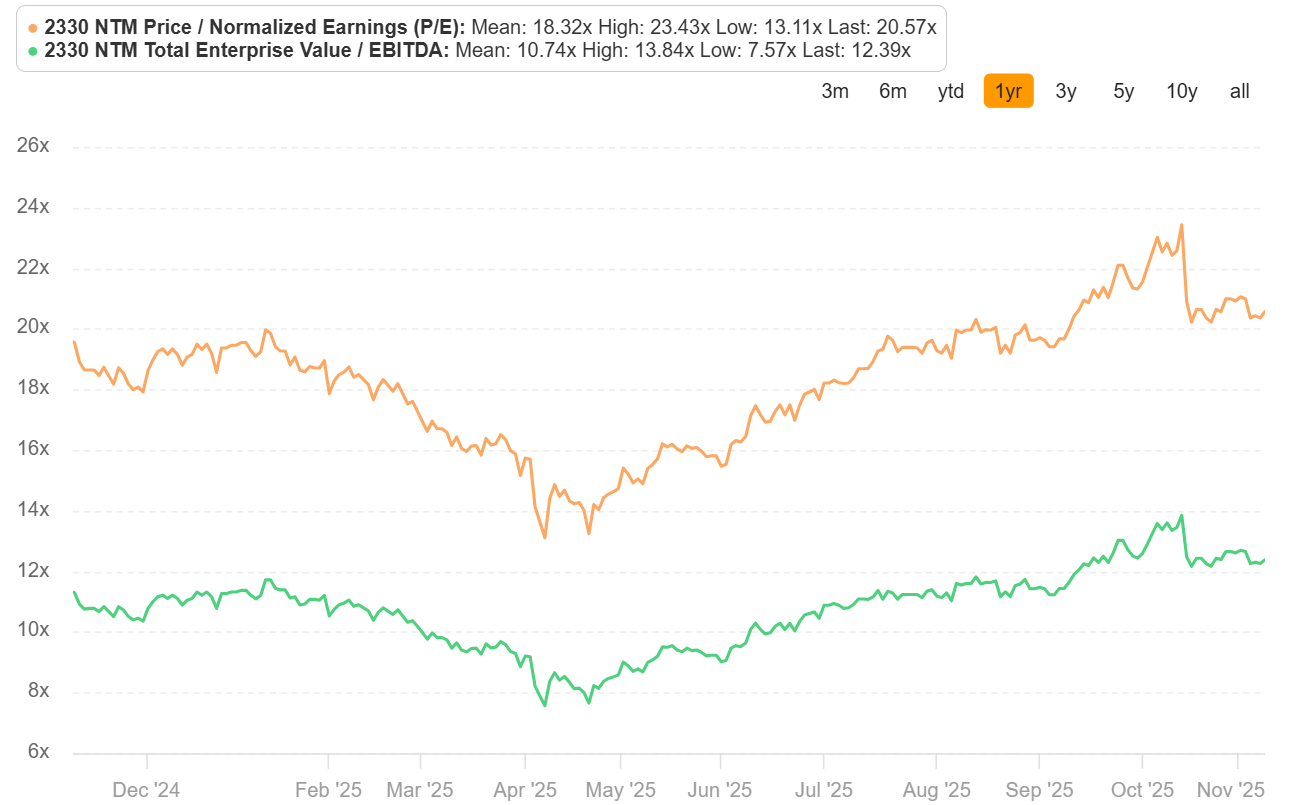

Current 4Q25 guidance is pointing to expected revenues of $32.8 billion at the midpoint, or +22% yoy, which is a meaningful slowdown from a +35% in Q1-25, a +47% in Q2-25 and a +41% in Q3-25, and this is the main reason affecting the current P/E NTM, which corrected downward to the current 20.6x from the yearly peak of 23.4x.

We believe however that the management’s projected revenue growth looks excessively prudent, in the light of the current trading (October monthly revenues increased by 11% m-o-m and, if confirmed for the next 2 months, will imply a 32% y-o-y growth in the Q4-25, far above company’s guidance and market consensus (pointing at a +24% growth).

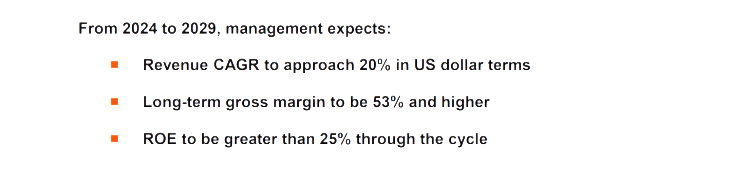

Similarly, at the beginning of the year, the management provided a mid-term revenue CAGR indication of 20% in US dollar terms. We believe that, given the current management indications, this estimates will be most likely significantly revised upward during the current next 2 quarters.

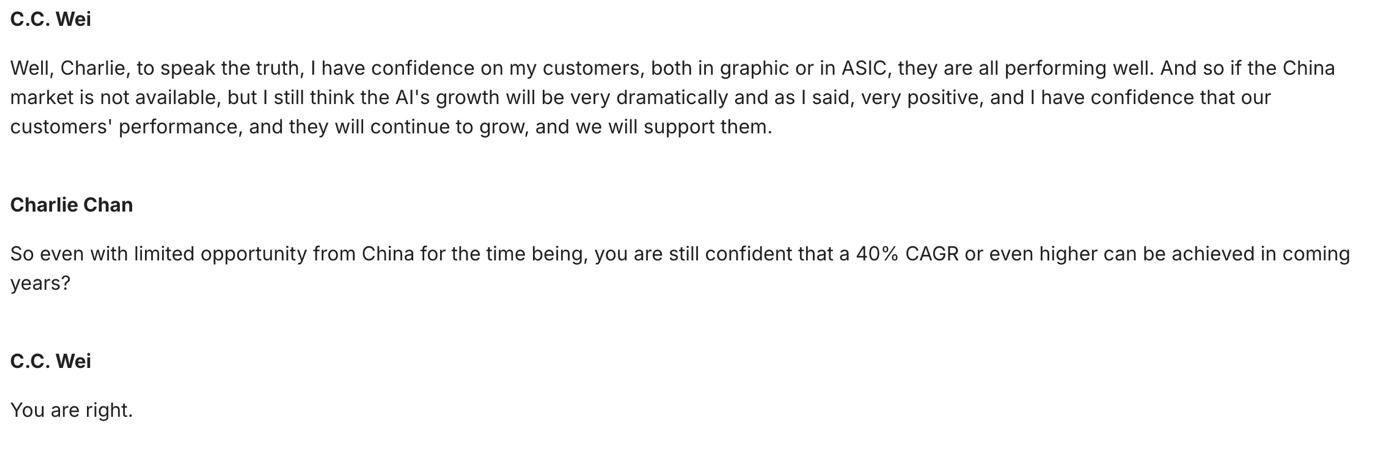

As a matter of fact, company’s management highlighted that AI business is supposed to grow at a CAGR of 40% in the coming years, with the reminder part of the business growing at a 20% CAGR.

Even in the event of a reduction in orders from one of its major clients, Nvidia, following its recent partnership with Intel aimed at diversifying part of its production, or a slowdown in the Chinese market due to trade tensions, TSMC’s management has reiterated that demand remains exceptionally strong – sufficient to sustain a CAGR of 40% or above over the coming years.

During the latest conference call, CEO C.C. Wei confirmed that demand related to artificial intelligence continues to exceed all expectations, describing it as “even stronger than we imagined just three months ago.”, also because of the exponential growth in tokens demand (unit elements of the AI large language models).

In the light of the above, considering that the AI business might be worth between 30% and 50% of the current consolidated revenues, it is likely that TSMC might update its future mid-term revenue growth guidance upwards to 30-35% (vs. 14% expected by market consensus).

Moreover, the country risk premium associated with Taiwan is gradually beginning to decline, as shown in the sovereign yield downward path, which should help to support higher multiples going forward. TSMC is also trying to diversify its production facilities abroad, in order to limit negative impacts from a potential China invasion of Taiwan.

Considering the above, we believe the combination of lower perceived risk on the country, an acceleration in growth and margins as well as a further US Dollar devaluation (negatively correlated to the Company’s trading multiples) should provide ground for a multiple re-rating, pushing the P/E NTM within the 25-30x region. Applying this multiple to projected earnings places the stock’s intrinsic value between $400 and $440 per ADR, a 44% upside from the current levels.